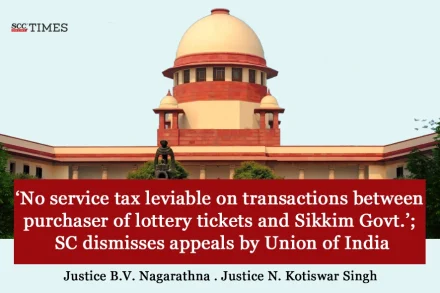

‘No service tax leviable on transactions between purchaser of lottery tickets and Sikkim Govt.’; SC dismisses appeals by Union of India

“There being no agency and no service rendered by the respondents-assessees herein as an agent to the Government of Sikkim, service tax is not leviable.”